KNOWLEDGE UNDERSTANDING AND ACCOUNTING PRACTICE SKILLS AFFECTING FINANCIAL REPORTING EFFICIENCY OF PERSONNEL UNDER THE ROYAL THAI POLICE

Article Sidebar

Main Article Content

Abstract

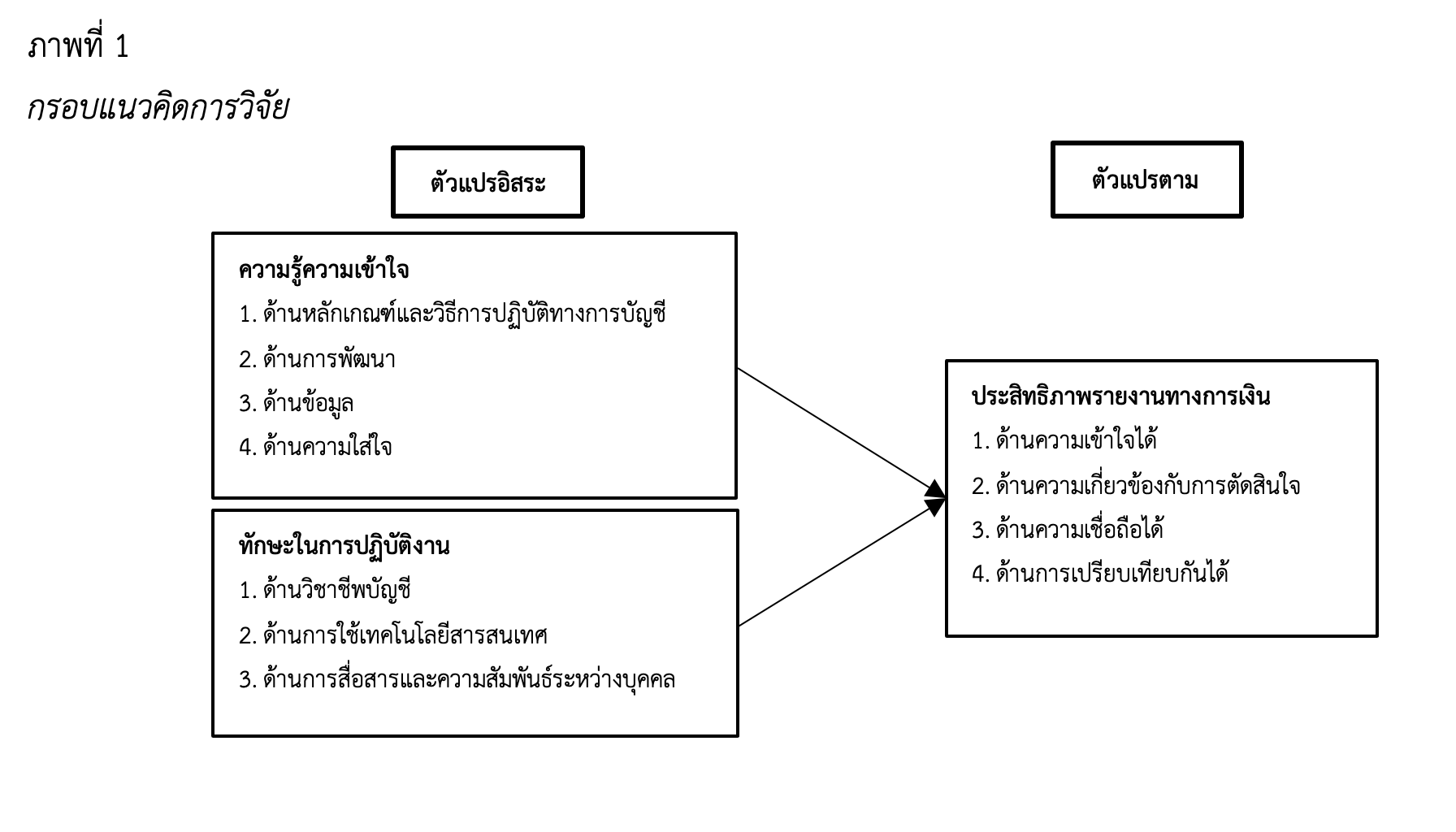

This study is a quantitative research methodology and aims to achieve two objectives. The first objective was to examine the impact of knowledge and understanding on the efficiency of financial reporting among personnel within the Royal Thai Police, and the second objective of this study was to examine the operational skills that impact the effectiveness of financial reporting among personnel within the Royal Thai Police. The data used in this study was obtained through the administration of a questionnaire to a sample of 113 individuals who held positions as police officers within the Accounting Division and Internal Audit Office. The data will undergo analysis utilizing descriptive statistics, including percentage calculations,

mean determination, standard deviation calculation, and correlation coefficient analysis. These techniques can be employed to examine the association between independent and dependent variables in order to ascertain the generalizability of the data. Furthermore, a multiple regression analysis was conducted to examine the research hypothesis at the 0.01 and 0.05 levels of statistical significance.

The results of the study indicate that:

There is a substantial positive relationship between information cognition, namely operational skills, communication, and interpersonal interactions, and the efficiency of financial reporting. This efficiency is measured in terms of understand ability (comprehension), decision-making relevance, reliability, and comparability. The statistical analysis confirms this relationship at a significant level of 0.01. Cognition and attentiveness had a positive effect on financial reporting efficiency, decision-making relevance, reliability, and understand ability (comprehension) at statistically significant levels of 0.01 and 0.05 respectively. However, it does not have an impact on the comparability skill. Cognition of accounting rules and practices had a statistically significant positive influence on the efficiency and reliability of financial reporting at the statistical significance level of 0.01, but had no effect on understand ability (comprehension), decision-making relevance, and comparability. Also, information technology, operational skills had a positive effect on financial reporting efficiency and comparable aspects at the statistical significance level of 0.05, but had no impact on understandability (comprehension), decision-making relevance, and reliability. Finally, this study concluded that cognition, skill development, namely operational skills and professional accounting practice had no effect on financial reporting performance in four dimensions, namely understandability (comprehension), decision-making relevance, reliability, and comparable aspects

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

The author(s) is only responsible for data appearing in the submitted manuscript of Interdisciplinary social sciences and communication journal.Besides, this journal encourages and enables you to share data such as statements, contents, figures, etc. that support your research publication where appropriate, and enables you to interlink the data with proper citation.

References

กรมบัญชีกลาง. (2563, 2 ตุลาคม). หนังสือกรมบัญชีกลาง ที่ กค 0410.2/ว479 ลงวันที่ 2 ตุลาคม 2563 เรื่อง รูปแบบการนำเสนอรายงานการเงินของหน่วยงานของรัฐ.

กรมพัฒนาธุรกิจการค้า. (2547, 5 สิงหาคม). ประกาศกรมพัฒนาธุรกิจการค้า เรื่อง กำหนดหลักเกณฑ์ วิธีการ และระยะเวลาในการพัฒนาความรู้ต่อเนื่องทางวิชาชีพของผู้ทำบัญชี พ.ศ. 2547

กรมวิชาการ. (2545). การวิจัยเพื่อพัฒนาการเรียนรู้ตามหลักสูตรการศึกษาขั้นพื้นฐาน.

กระทรวงการคลัง. (2564, 20 เมษายน). ประกาศกระทรวงการคลัง เรื่อง มาตรฐานการบัญชีภาครัฐและนโยบายการบัญชี ภาครัฐ (ฉบับที่ 2) พ.ศ. 2564.

กรรณิกา เหมือนรักษา. (2565). การเพิ่มประสิทธิภาพในการจัดทำรายงานการเงินของสำนักงานตำรวจแห่งชาติ. เอกสารศึกษาหลักสูตรการบริหารงานตำรวจชั้นสูง รุ่นที่ 51, วิทยาลัยการตำรวจ

กองอัตรากำลัง สำนักงานกำลังพล. (2564). คุณสมบัติเฉพาะตำแหน่งข้าราชการตำรวจ กลุ่มงานบริหาร กลุ่มงานอำนวยการและสนับสนุนและกลุ่มงานเทคนิค (ฉบับปรับปรุง พ.ศ. 2564).

กัลย์ธีรา สุทธิญาณวิมล. (2552). ปัจจัยที่มีผลต่อคุณภาพงบการเงินของวิสาหกิจขนาดกลางและขนาดย่อมในมุมมองของผู้สอบบัญชีรับอนุญาตในเขตภาคเหนือ. [การค้นคว้าอิสระปริญญามหาบัณฑิต ไม่ได้ตีพิมพ์]. มหาวิทยาลัยเชียงใหม่.

กุลวดี ลิ่มอุสันโน. (2559). ความรู้ความเข้าใจของนักบัญชีไทยต่อมาตรฐานการรายงานการเงินสำหรับธุรกิจขนาดกลางและขนาดย่อมในประเทศไทย. รายงานวิจัย, มหาวิทยาลัยสงขลานครินทร์.

สำนักงานคณะกรรมการพัฒนาระบบราชการ (ก.พ.ร.). (2562). เกณฑ์คุณภาพการบริหารจัดการภาครัฐ. สำนักงานคณะกรรมการพัฒนาระบบราชการ.

จิรภัทร์ มั่นคง. (2561). ปัจจัยด้านความรู้ความสามารถของข้าราชการและพนักงานการเงินและบัญชีกรมการเงินทหารบกที่มีอิทธิพลต่อคุณภาพข้อมูลทางการเงิน. [การค้นคว้าอิสระปริญญามหาบัณฑิต ไม่ได้ตีพิมพ์]. มหาวิทยาลัยศรีปทุม.

ณพนณัฐ คำมุงคุณและกนกศักดิ์ สุขวัฒนาสินิทธิ. (2566). สมรรถนะของนักบัญชีและการยอมรับนวัตกรรมการบัญชีส่งผลกระทบต่อประสิทธิภาพของรายงานทางการเงินในเขตภาคตะวันออก. วารสาร มจร. อุบลปริทรรศน์, 8(1), 159-169.

นันท์นภัส รักเดชะ. (2563). คุณลักษณะและประสิทธิภาพการปฏิบัติงานของผู้จัดทำบัญชีภาครัฐที่มีผลต่อคุณภาพรายงานการเงินขององค์กรปกครองส่วนท้องถิ่นในเขตภาคใต้ของประเทศไทย. [การค้นคว้าอิสระปริญญามหาบัณฑิต ไม่ได้ ตีพิมพ์]. มหาวิทยาลัยศรีปทุม.

นภา จันทรา. (2557). ความรู้และความเข้าใจของผู้ทำบัญชีในจังหวัดเชียงใหม่เกี่ยวกับมาตรฐานการรายงานทางการเงินสำหรับกิจการที่ไม่มีส่วนได้เสีย. [การค้นคว้าอิสระปริญญามหาบัณฑิต ไม่ได้ตีพิมพ์]. มหาวิทยาลัยเชียงใหม่.

ประภาศรี เหลือถนอม. (2557). ผลกระทบของกระบวนการจัดทำบัญชีที่มีต่อประสิทธิภาพรายงานทางการเงินของสหกรณ์ในเขตภาคตะวันออกเฉียงเหนือ. [วิทยานิพนธ์ปริญญามหาบัณฑิต]. มหาวิทยาลัยมหาสารคาม.

พระราชกฤษฎีกาแบ่งส่วนราชการสำนักงานตำรวจแห่งชาติ พ.ศ. 2552. (6 กันยายน 2552). ราชกิจจานุเบกษา. เล่ม 126 ตอนที่ 65 ก หน้า 1-18.

พระราชกฤษฎีกาว่าด้วยหลักเกณฑ์และวิธีการบริหารกิจการบ้านเมืองที่ดี พ.ศ. 2546. (9 ตุลาคม 2546). ราชกิจจานุเบกษา. เล่ม 120 ตอนที่ 100 ก หน้า 1-14.

พระราชบัญญัติตำรวจแห่งชาติ พ.ศ. 2565. (16 ตุลาคม 2565).ราชกิจจานุเบกษา. เล่ม 139 ตอน ที่ 64 ก หน้า 1-80.

พระราชบัญญัติระเบียบบริหารราชการแผ่นดิน (ฉบับที่ 5) พ.ศ. 2545. (2 ตุลาคม 2545). ราชกิจจานุเบกษา. เล่ม 119 ตอนที่ 99 ก หน้า 1-13.

พระราชบัญญัติวินัยการเงินการคลังของรัฐ พ.ศ. 2561. (19 เมษายน 2561). ราชกิจจานุเบกษา. เล่ม 135 ตอนที่ 27 ก หน้า 1-22.

ภัทราพร อุระวงษ์. (2563). ทักษะการปฏิสัมพันธ์และการสื่อสาร ที่มีต่อผลการปฏิบัติงานทางบัญชีของนักบัญชีในเขตกรุงเทพมหานคร. [การค้นคว้าอิสระปริญญามหาบัณฑิต ไม่ได้ตีพิมพ์]., มหาวิทยาลัยศรีปทุม.

ราชบัณฑิตยสถาน. (2554). พจนานุกรม ฉบับราชบัณฑิตยสถาน พ.ศ. 2554. https://dictionary.orst.go.th/index.php

สภาวิชาชีพบัญชี ในพระบรมราชูปถัมภ์. (2566). มาตรฐานการศึกษาระหว่างประเทศสำหรับผู้ประกอบวิชาชีพบัญชี (ฉบับปรับปรุง Volume 2015) ฉบับที่ 3 (ฉบับปรับปรุง) เรื่อง การพัฒนาทางวิชาชีพระยะเริ่มแรก – ทักษะทางวิชาชีพ. https://www.tfac.or.th/upload/9414/eq6p8RJwV0.pdf

สมใจ ลักษณะ. (2552). การพัฒนาประสิทธิภาพในการทำงาน. เพิ่มทรัพย์การพิมพ์.

สมชาย บุญศรี. (2559). ความรู้ความเข้าใจเกี่ยวกับการใช้สิทธิประโยชน์ 7 กรณีของผู้ประกันตนที่มาใช้บริการสำนักงานประกันสังคมจังหวัดชลบุรี. [วิทยานิพนธ์ปริญญามหาบัณฑิต]. มหาวิทยาลัยบูรพา.

สุวิมล ติรกานันท์. (2546). ระเบียบวิธีการวิจัยทางสังคมศาสตร์ : แนวทางสู่การปฏิบัติ. โรงพิมพ์แห่งจุฬาลงกรณ์มหาวิทยาลัย.

อภิชาติ อนุกูลเวช. (2551). การพัฒนารูปแบบการเรียนการสอนฝึกปฏิบัติทางเทคนิคบนเครือข่ายอินเทอร์เน็ตสำหรับนักเรียนอาชีวศึกษา. [วิทยานิพนธ์ปริญญาดุษฎีบัณฑิต]. มหาวิทยาลัยศรีนครินทรวิโรฒ.

Gagne', Robert M. & Briggs, Leslie J. (1979). Principles of instructional design (2nd ed). Holt, Rinehart and Winston.

Hinkle, D.E. (1998). Applied Statistics for the Behavioral Sciences. Houghton Mifflin.

Millet, John D. (1954). Management in the Public Sector: The Quest for Effective Performance.McGraw-Hill Book Company.

Gagne, Robert M. (1970). The Condition of Learning. Holt, Rinchart and Winston.

Yamane, T. (1973). Statistics: An Introductory Analysis (3 edition) . Harper and Row Publication.